Did you know that within 15 years Social Security will not be able to pay out all of its promised retirement benefits? This is bad, but the news got a bit worse this week. The federal government now reports that for the first time in over 35 years, Social Security will have to dip into its reserves to pay out retirement benefits.

We Knew It Was Coming

This isn’t as shocking as it might seem on the surface, but it’s not good news either. The projection had always been that Social Security would not be able to pay out benefits from inflows coming in. But the big news here is that this happened three years earlier than anybody expected.

The problem is that now there are not enough workers paying Social Security taxes to pay benefits to the huge number of baby boomers receiving Social Security now. This will get worse over the next 20 years, which is why Social Security will not be able to meet its obligations within 15 years.

In order to understand why this is such a problem, we need to also understand where Social Security gets its money and how it funds the trust fund.

As most workers know, there is a 6.2% tax on earnings for the employee. Employers also pay that exact same amount for each employee they have. The maximum amount that can be taxed this year is $128,400.

For the self-employed, Social Security taxes are one of the most painful taxes to pay. That is because those who are self-employed are both employer and employee. Therefore they pay the full 12.4% of their income.

Now we know where the money for Social Security is coming from. But most of it goes right back out the door to pay for Social Security benefits to retirees today. Any amount left over goes into a fund to pay for future benefits. From now on there will be no leftover amount that funds anything.

It is this fund that is now being tapped to help cover shortfalls. This fund is projected to hit $0 in 2034, at which point the inflows coming in from Social Security taxes will only cover about 75% of the benefits being paid out. This is when cuts will have to be made or Congress will have to find another huge source of income to pay out the benefits.

What You Can Do

It’s very likely that Congress will do nothing to shore up Social Security until the absolute last minute. So it’s best to assume that when the time comes, they will panic and cut benefits for those with higher income and/or assets. They might also increase the age at which we can take our Social Security benefits.

It is very important that we all know how different scenarios might play out for our retirement plan. The best way for the do-it-yourself type to project how cuts to Social Security might play out is to use planning software such as WealthTrace.

Running What-If Scenarios

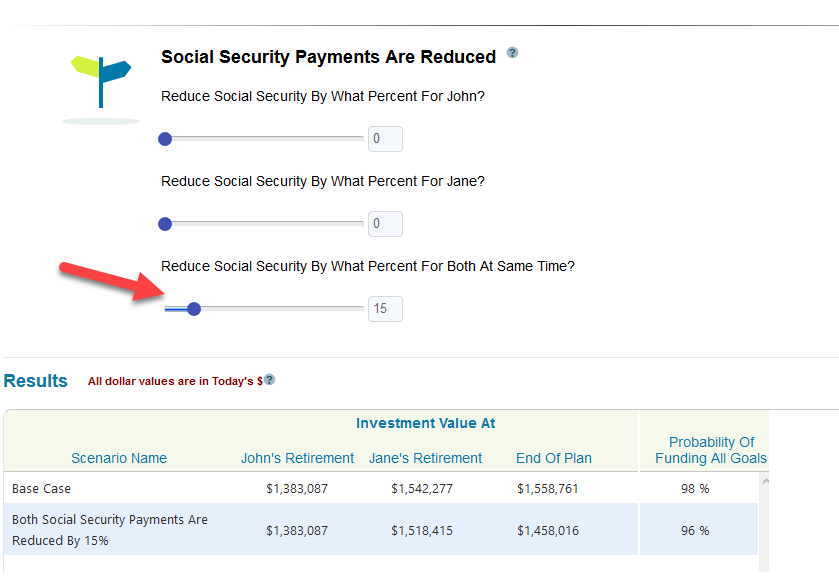

How important are Social Security benefits to your retirement plan? What if your benefits are cut by 15%? Very few can answer this question off the top of their head. By we can run a lot of different what-if scenarios in the WealthTrace Retirement Planner and see how this impacts any retirement plan.

I ran a Social Security scenario, as you can see above. In this scenario, I reduced their Social Security benefits by 15% annually. You can see the impact that this has on their plan. The money they have left at the end of their plan (when both people have passed away) is about $100,000 less. Also, their probability of plan success goes from 98% to 96%. This isn’t a huge impact, but it depends on one’s financial situation. If you’re very dependent on Social Security to cover expenses, the impact will be greater.

Other Things You Can Do

As I mentioned previously, it is best to assume that you will not receive your full Social Security benefits if you have a good income level or level of assets. If you plan on retiring with more than $1 million in assets, the federal government will probably tell you that you don’t need all of the benefits you were promised.

So take things into your own hands. Max out your 401(k) plan if you have one at work. There aren’t many better ways to save than a 401(k) plan, especially if your employer matches some of your contributions.

You should also look at solid dividend-paying stocks that can help provide enough income in retirement to cover your expenses, even if Social Security benefits are cut. The best way to ensure you don’t run out of money in retirement is to have enough income to cover your retirement expenses every year.