According to a recent article from MagnifyMoney, applying for a credit card will lower your credit score by 5-10 points.

You want to avoid that kind of damage.

Annoyingly enough, the more you apply for credit cards, the less likely you are to get one because of the damage you’re doing to your score. The goal of this post is to help you know if you’ll be approved – before even applying. Aim for a 1:1 ratio. For every one card you apply for, you should receive one card.

I got my first card card recently and it’s a great one! Here’s what I did:

Step #1: Find out What You Really Want

Before you determine whether or not you should be qualified for a card, you need to gather a list of cards you want.

To start your search, think about why you want a credit card in the first place. Are you looking to build credit? Do you want cash rewards? Do you need a low interest rate? Google, ‘Best cash back/interest rate/credit building credit cards of 2015.’ Check a few sites and cross-reference them. If 3-4 reputable sites believe a card is good, it probably is good. Create a list of at least 3 cards you would like to have.

Step #2: Check Your Credit Reports

You are allowed to view your credit reports for free once a year. The only site you can do this from is annualcreditreport.com. Pull your reports from Equifax, TransUnion, and Experian. The process is straightforward. It should take you about 15 minutes to get all your reports. Review them and see if there’s anything out of place. Check what physical address is listed. See if your loan history looks familiar.

These credit reports are what credit card companies use to approve or deny you. You want them to be accurate so you’re not denied for invalid reasons.

Step #3: Check Your Credit Score

After being on annualcreditreport.com you will have seen an upsell to check your credit score. This is because the credit score doesn’t appear anywhere on your credit reports. The upsell is about $40 extra. Good news, however – you don’t need to buy a credit score. There are several ways to obtain it for free. My preferred method (which I used one week ago) is by checking my Mint.com account. It displays a free FICO score.

Once you have your credit reports and your credit score, you have all the raw data you need to determine if you will be approved or denied.

Step #4: See What Credit Score You Need

To preface this step, FICO credit scores are not the be-all and end-all to getting approved or denied. It’s just a helpful indicator as to the overall health of your credit.

Most cards say they are for people with ‘poor.’ ‘good,’ ‘fair,’ ‘average,’ ‘rebuilding,’ ‘good,’ or ‘excellent,’ credit. These words don’t really mean much. Obviously, if you are new to credit cards you should not go after one which says it’s for people with excellent credit. However, don’t get too caught up with these words.

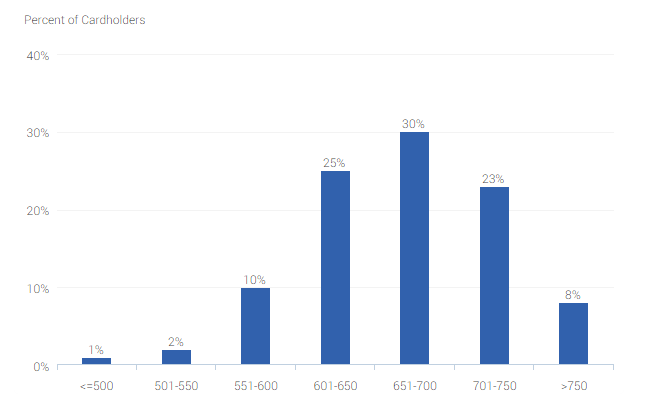

Instead, see what credit score range you need to get accepted. Credit card reviews on CreditKarma.com will give you a good idea of what score you should have. The example is for a Discover it card:

Step #5: Try to Get Pre-Approved

Getting pre-approved for a credit card isn’t as easy as you may think. Unless the company sends you letters telling you that you’re pre-approved, the pre-approval process isn’t as glamorous as it sounds. First of all, there are very few credit card sites that will give you the pre-approval nod. Here are ones that do:

It’s a short list. And be careful. Some sites will say, ‘We couldn’t find any cards specifically for you but we think you’ll like these.’ That’s their way of saying, “No, we won’t give you credit. But we still want you to apply so we can get your information in case we want to solicit you in the future if your credit does improve.”

Although I would like to be able to tell you that you could always just get pre-approved in 10 seconds, it’s generally not that easy.

Also, getting pre-approved doesn’t harm your score at all.

Step #6: Do any of these other credit problems apply to you?

If you have any of these issues, you may get denied:

1) There’s a gap in your credit history

2) You’re using a good amount of credit already

That’s right, even if you are a responsible credit card user with an 800+ credit score, you can still be denied for the reasons listed above. It’s hard to measure these risks. Just be aware that you have a lower chance of getting approved if either of these apply to you.

Step #7: You Never Fully Know until You Apply

You can (and should) consider all the steps above. However, you never know for certain until you apply. If you follow this post, you’ll probably get approved for whatever card you choose. However, if you do apply and get denied, the credit card company will tell you why. Before you lose another 5-10 points from your FICO score, rethink your next application. You can either try for a similar credit card from another company or you can apply for an easier to obtain credit card such as a secured credit card.

For More On Credit Cards and Credit

Using this guide will help you ‘get approved’ without even applying. Once you go through the application process, you shouldn’t get a major surprise. If you are looking to learn more about credit and credit cards I recommend that you pick up a copy of Dave Ramsey’s The Total Money Makeover or a copy of Suze Orman’s The Road to Wealth

. Both of these books are solid, reliable texts which contain good advice. They’ve both sold millions of copies, so you won’t go wrong with them.

I’m a personal finance freelance writer and webmaster. I welcome you to visit me at www.thefrugalpreneur.com